Qualified Small Business Stock (QSBS) - Just Got Better: What Founders Need to Know Now

When founders think about building wealth through startups, Qualified Small Business Stock (QSBS) under Section 1202 of the Internal Revenue Code has long been one of the most powerful tax planning tools available. But with the recent passage of the One Big Beautiful Bill Act (OBBBA) on July 4, 2025, things just got even better for startup founders, investors, and early employees.

Here’s a breakdown of what changed — and what it means for you.

A Quick Refresher: What Is QSBS?

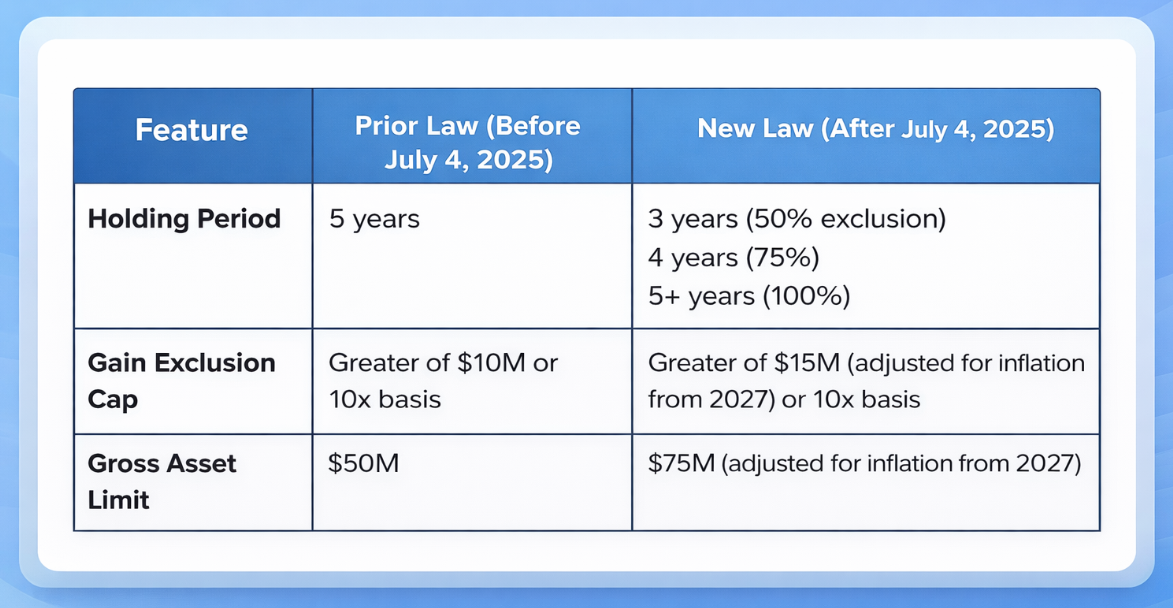

QSBS is a special class of stock issued by qualified C-corporations that allows for partial or full exclusion of capital gains from federal income tax when the stock is sold. For years, founders and early investors who met certain requirements could exclude up to 100% of their gains — up to $10 million or 10x their basis — if they held the stock for at least five years. Check out this Fourscore primer for more information on QSBS Basics.

The OBBBA’s Major QSBS Upgrades

The OBBBA changes three core components of QSBS for stock acquired after July 4, 2025:

TL;DR: More companies qualify, the benefit is available sooner, and the cap is higher.

Founder Scenario: How One Founder’s Tax Bill Just Got Way Smaller

Taylor, a first-time founder who incorporated their Delaware C-Corp in August 2025 received common stock in exchange for IP and services. Imagine that Taylor raises a $2M seed round in December and plans for a Series A in late 2026. After selling the company in mid-2029, here’s what QSBS treatment looks like:

Holding Period: 4 years (falls between 3–5 years)

Gain on Exit: $6 million

QSBS Status: 75% exclusion

Under prior QSBS rules, Taylor wouldn’t have hit the 5-year mark and would have owed capital gains taxes on the full amount. Now, under OBBBA’s tiered system, they qualify for a 75% exclusion — paying tax only on $1.5 million of the gain instead of the full $6 million. That’s a potential tax savings of over $1 million, depending on their personal tax rate.

Strategic Planning Considerations for Founders

If you’re a founder raising or issuing equity after July 4, 2025, these changes open new planning opportunities:

Earlier Liquidity Events: You may not need to wait 5+ years to sell and still enjoy substantial tax savings.

More Room for Growth: Higher gross asset limits mean more later-stage companies may still qualify.

Cap Table Management: Coordinate QSBS eligibility with early employees and investors — good planning can significantly impact everyone's post-exit outcomes.

Entity Formation Timing: If you’re still on the sidelines about incorporating, now may be a great time to form your C-Corp.

What You Can’t Do: Beware of QSBS "Refresh" Loopholes

The OBBBA also closes potential loopholes by disallowing “refresh” strategies, such as trying to swap old QSBS for new shares after July 4, 2025 to take advantage of the new rules. The acquisition date rules emphasize that only newly issued shares after July 4, 2025, count for the enhanced benefits — not stock swapped in tax-deferred deals.

Final Thoughts

The QSBS changes under the OBBBA make it an even more attractive vehicle for founders and early stakeholders to build tax-efficient wealth — but only with thoughtful corporate legal and tax planning. Whether you're launching a new startup, issuing founder stock, or preparing for a fundraising round, it’s time to revisit your QSBS strategy.

Need help navigating the new rules? Fourscore’s team is ready to advise you and your startup. We help founders make informed decisions that protect long-term upside. Book a call today.

Related Posts

Conversations with AI May Not Be Confidential

Business owners should be careful using consumer AI tools for legal questions: prompts may not be confidential, could be discoverable in litigation, and don’t replace attorney-client privilege or professional legal counsel.

Technology

Entrepreneurship

Building a Culture That Lasts: Leadership, Growth, and the Discipline of Rest

Leadership isn’t just about growth or hard work — it’s about building trust, empowering your team, and modeling rest to create a healthy culture that lasts.

Entrepreneurship

Technology

Social

Automation for Founders in the Investment Stage

Unlock exponential growth. 🚀 Learn how venture-backed founders use automation to stop being bottlenecks and start scaling. From QA as a trust metric to data pipelines, build the "machine" that drives your vision toward Series A. Read more here.

Entrepreneurship

Technology